Melvyn Wilson

Melvyn Wilson

Energy market update: What UK businesses need to know this week

Energy markets are riding a rollercoaster in 2026 - and your business is paying for it.

Energy markets continue to be dominated by escalating and unresolved geopolitical risk in the Middle East, with the Strait of Hormuz remaining the central structural concern.

Price volatility has continued throughout April driven by on-off peace talks and political rhetoric. Currently, diplomatic progress has stalled but this can change quite quickly.

However, market focus has shifted away from short term headlines toward the duration of disruption, infrastructure damage, and long-term LNG supply losses, fundamentally tightening the global gas outlook into the late 2020s according to the latest International Energy Agency analysis.

What began as a short-term geopolitical shock is now locking in multi year LNG supply losses, prolonged shipping risk, and lasting damage to confidence in global energy transit.

Price formation is no longer driven primarily by weather or storage, but by geopolitical duration, infrastructure repair timelines.

The balance of risk therefore remains on the upside with limited downside forecasted, and heightened volatility into winter and beyond.

Currently market prices after 2026 and early 2027 remain lower (backdated) and have not seen the same impact as the near term.

However, the longer the conflict continues we may see sentiment shift from the 2026 period into Summer and Winter 2027 and longer dated contracts.

Structural supply issues - Lost LNG volumes, especially from Qatar, cannot be replaced quickly.

Low storage levels - EU storage is sitting around 35%, well below last year.

Ongoing volatility - Prices are moving sharply week-to-week.

Rising non-commodity costs - With higher transmission cost and other green taxes increases expected through 2030.

Analysts do not see wholesale prices dropping significantly in 2026 even if the conflict is resolved with expectation they may rise further with market analysts modelling gas prices in the £38 - £70MWh (3.8p - 7pKwh) for this year depending on the duration of conflict.

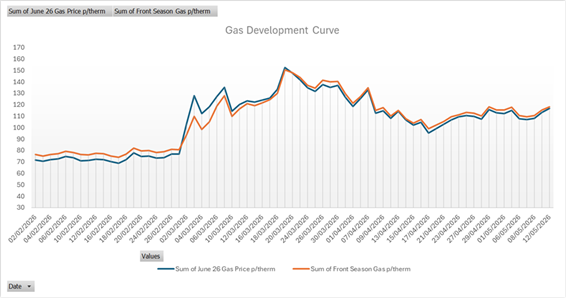

The impact of the US-Iran conflict can be seen from the end of February.

Business energy is confusing. You know you need to stay on top of such a major cost, but that can be difficult while focusing on running your business and serving your customers.

We get it. We can support you.

Troo exists to help businesses like yours make sense of their energy needs, simplify complex information and make smart decisions that lead to real change and reduced costs.

Book a free energy health check today for practical guidance on your business electricity, gas or water bills.

We are not here to sell you a quick fix. We're here to understand what matters to you, offer clear advice, and take ownership of the hard parts, so energy becomes one less thing to worry about.

Energy markets are riding a rollercoaster in 2026 - and your business is paying for it.

You didn't go into business to become an expert in business energy. In 2026, it feels like you need to be one.

You have probably paid Value Added Tax (VAT) on something already today.